- Inflation concerns fade as Fed officials stay with the dovish theme.

- Oil takes flight as the Suez remains blocked.

- Stocks close out the week in the green but big tech struggles.

Equities close nicely on Friday to cap a solid week of gains for the broader indices. The S&P 500 finished the week ahead by 1.57%, The Dow is positive for the week up 1.36% but the Nasdaq trails behind, losing 0.59% for the week.

Big tech has had a subdued time as the rotation into more cyclical stocks continues. Financial stocks had been helped on Friday as the Federal Reserve said it will lift restrictions on dividends and buybacks in June. The S&P 500 set a record high close, not a record high, as it took out the St. Patrick’s day close by half a point!

Meme stocks retook the narrative on Thursday, posting enormous gains of over 50% for Gamestop and KOSS with nearly 30% for AMC.

SPAC’s suffered as the SEC looks into some recent SPAC deals, CCIV finished the week at $23.02.

Stay up to speed with hot stocks’ news!

Friday saw a string of positive data to boost equity sentiment. Personal Consumer Expenditures (PCE) deflator helped calm inflation fears and the Michigan Consumer Sentiment data showed continued growth. The US 10-year yield remained under 1.7% as Fed officials continued their dovish testimony throughout the week.

The Dollar remained strong taking out another big figure during the week to trade with a 1.17 handle. Interest rate differential and EU economic and vaccine woes continue to be the main drivers of the strong dollar.

Oil prices drove higher on Friday, despite the dollar strength and EU demand headwinds. The continued Suez canal blockage and rumours of OPEC+ not increasing production in April boosted oil to close 4% higher on Friday at $60.81. The contango effect also lessened as the week progressed.

S&P 500 Week Ahead

Equities have struggled this week but still made progress, albeit slowly. Fundamentals continue to favour higher prices in the week ahead. Bank of America’s money flow data this week was bearish with near record inflows to short-term treasury funds and cash. This will return as long as equities can remain bid and yields stay under control. Stimulus checks still haven’t fully made their way into the market and President Biden’s infrastructure plan is also underpinning industrial stocks. Despite stretched valuations, the rally may continue a while yet.

Clocks move one hour forward this weekend in Europe to summertime. GMT +1 for the UK, GMT +2 for Europe.

Monday sees the Dallas Fed Manufacturing Index, coming in at 17.2 in February. Monday also sees 3 and 6 month Bill auctions. Federal Reserve member Christopher Waller speaks at 1100EST/1500GMT.

On Tuesday, the US Consumer Confidence data is expected to show continued improvement as stimulus checks and reopening flow through to consumers.

Europe releases German CPI but European inflation is not a focus for equity markets currently.

Wednesday has mortgage applications and Chicago PMI. PMI is expected to come in at 60.3, a rise from 59. President Biden is also due to speak on Wednesday.

Thursday closes out the short Easter week with ISM Manufacturing data. The focus will be on the New Orders component and the PMI. PMI is expected to show a continued gain to 61.2. Construction spending is also out on Thursday but won’t show improvement yet as lockdown still affects the number. Next month will be more important.

OPEC also meets on Thursday so keep an eye out for any commentary on supply. Hopefully, the Suez canal is open by then!

Earnings due

Blackberry releases earnings on Tuesday. One of the meme stocks, it is expected to report EPS of $0.03 and revenue of $246.36 million.

Lululemon Athletica also releases on Tuesday, EPS expected to be $2.49 and revenue of $1.66 billion.

McCormick & Co gets Q1 out early, expected EPS is $0.58 and revenue of $1.37 billion.

Walgreens Boots Alliance reports Wednesday, EPS expected to be $1.12 and revenue of $35.46 billion. Walgreens may comment on covid vaccine rates as they have been participating.

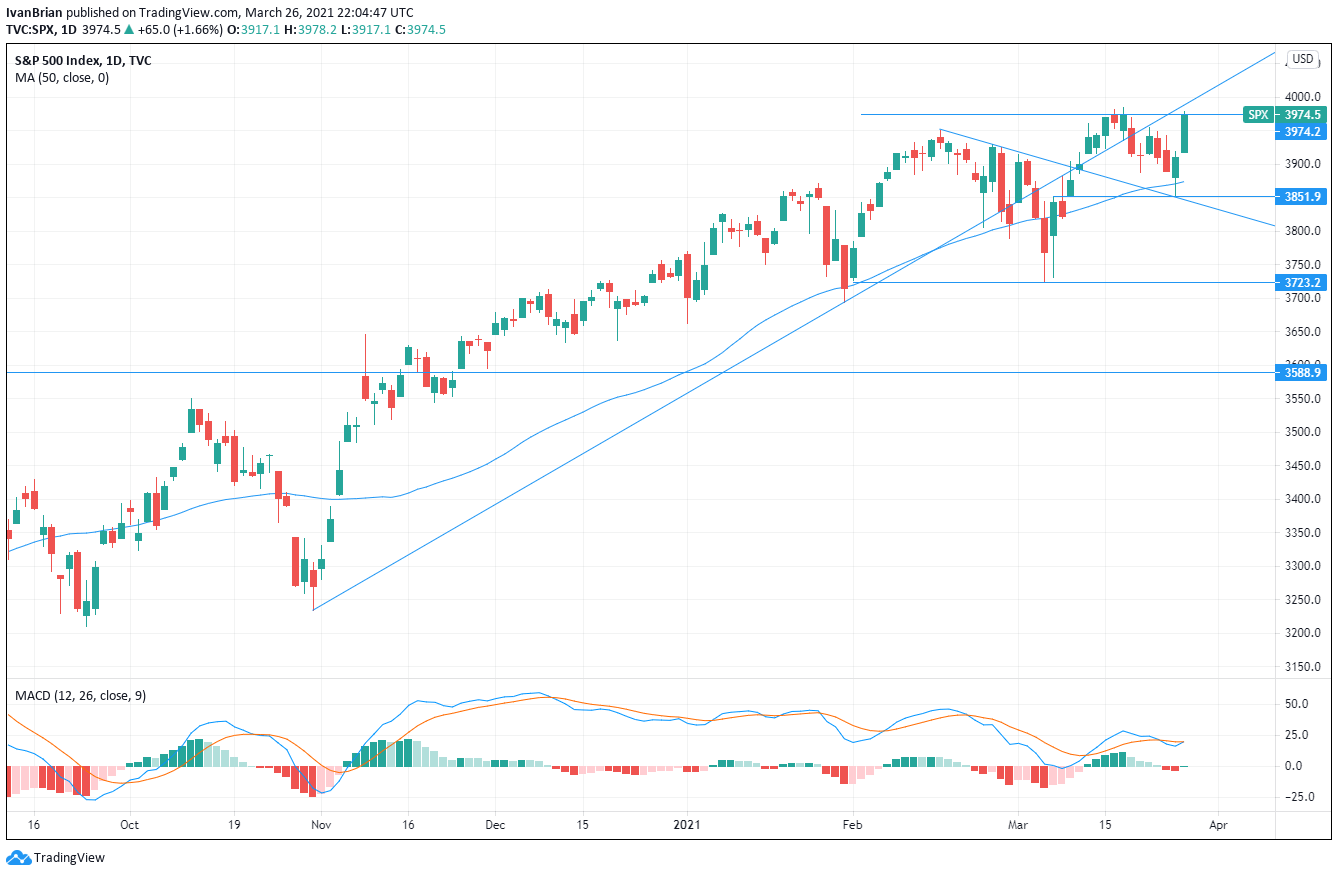

S&P 500 technical analysis

Decision time beckons on Monday. The S&P rallied into the close on Friday to set up for a record close and just missing the March 17 record high. The 50 day moving average worked for a near perfect support to kick start the rally on Thursday. Stimulus checks and investors’ funds look likely to push equities higher ahead of the Easter break. Key support at 3851.

The author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

This article is for information purposes only. The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice. It is important to perform your own research before making any investment and take independent advice from a registered investment advisor.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to accuracy, completeness, or the suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. The author will not be held responsible for information that is found at the end of links posted on this page.

Errors and omissions excepted.